108: Berkshire's Not-So-Concentrated Equity Portfolio & Valuation Update

A business is a stock is a business.

You’re reading the free version of Watchlist Investing on Substack. If you’re not already subscribed, click here to join 2,800 others.

Want more in-depth and focused analysis on good businesses? Check out some sample issues of Watchlist Investing Deep Dives, a separate paid service.

For $20.75 per month, you can join corporate executives, professional money managers, and students of value investing receiving 10-12 issues per year. In addition, you’ll gain access to the archives, now 30 issues and growing!

To Concentrate Or Not Concentrate, That Is The Question

Tis nobler to concentrate one’s investments in a few companies. That’s the Buffett cum Shakespeare paraphrasing that value investors and the business press love to tout. And it’s true, just not so much today and not in the context of the whole of Berkshire.

Many journalists commented on the fact that 78% of Berkshire’s equity portfolio was concentrated in just five companies:

Apple (48.9%)

Bank of America (8.6%)

American Express (6.8%)

Coca-Cola (6.4%)

Chevron (4.4%)

At the 2023 BRK AGM, Becky Quick asked a question from a shareholder who noted that Aswath Damodaran, a respected (me included) professor at NYU, thought Berkshire’s concentration in Apple was “dangerous”.

Not surprisingly, Buffett and Munger had a different take.

CHARLIE MUNGER: I think he’s out of his mind.

WARREN BUFFETT: Yeah, I knew that was coming. (Laughter) Apple is not 35% of Berkshire’s portfolio. Berkshire’s portfolio includes the railroad, the energy business, Garanimals, you name it, See’s Candies, they’re all businesses. And, you know, the good thing about Apple is that we can go up.

Sure, Apple is a large position, worth $157 billion as of the end of Q3-2023. But it’s only about 15% of my estimated value of Berkshire Hathaway (adjusted for my estimate of Apple’s value, which is lower). As Buffett noted, Berkshire’s wholly-owned businesses are 100% positions in stocks. On that basis Berkshire is far more diversified.

And they can’t own more than 100% of the railroad. But it delights Buffett to be able to own more of Apple, either through direct purchases or indirectly as Apple repurchases shares.

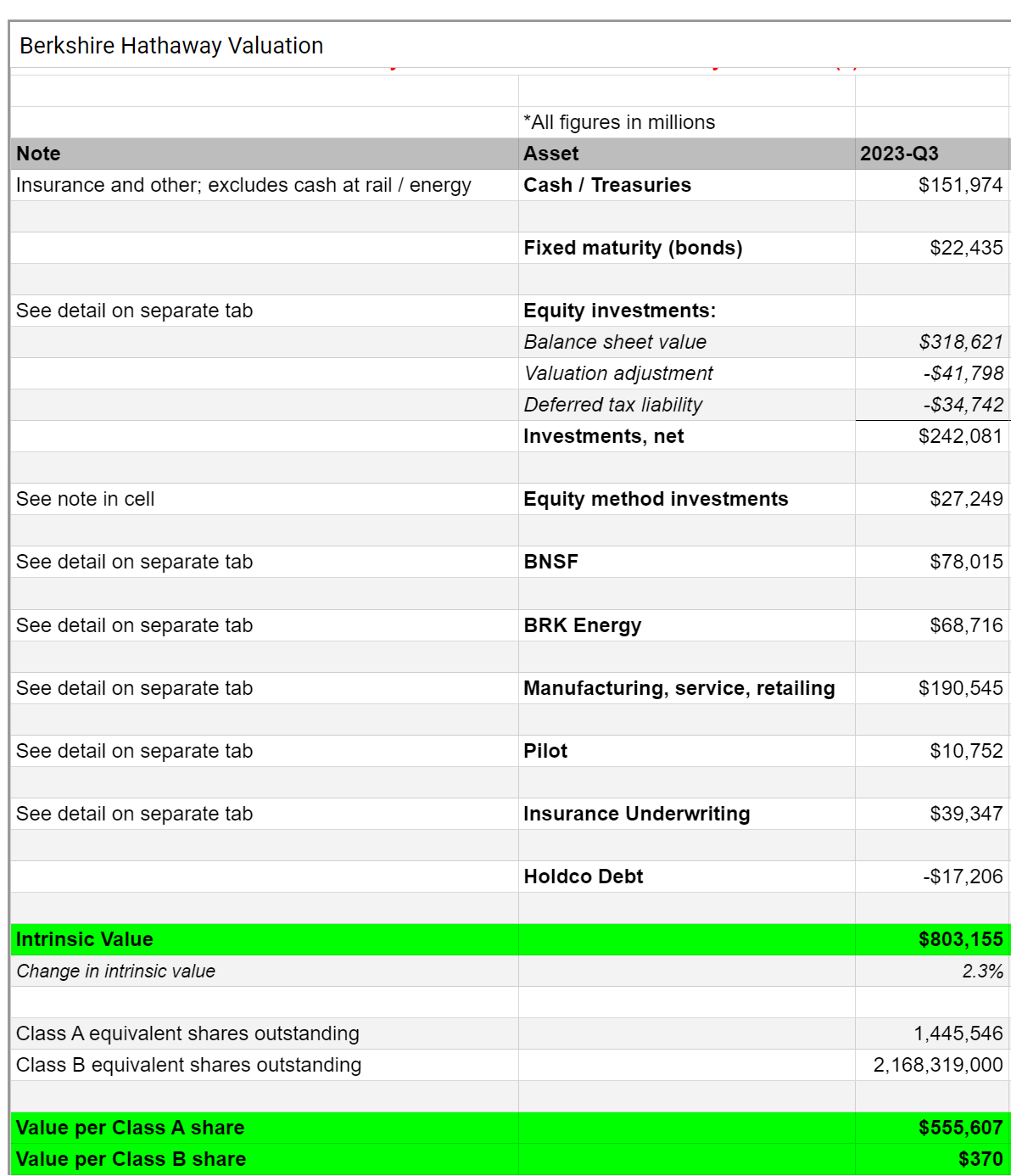

Below is a snapshot of my latest valuation overview of Berkshire. Paid Deep Dives subscribers have access to the live Google Sheet which contains details on each section. They also received my latest 2-page analysis commenting on Berkshire’s Q3 results.

Stay rational! —Adam

$78B seems like a very conservative price for BNSF? Do you expand upon the valuation adjustment within the equity portfolio to paid subscribers? I'm going to buy your book on Berkshire and am considering paying for a subscription.