115: Mainfreight, Ltd.

A New Zealand-based logistics company with worldwide ambitions.

You’re reading the free version of Watchlist Investing on Substack. If you’re not already subscribed, click here to join 3,000 others.

Want more in-depth and focused analysis on good businesses? Check out some sample issues of Watchlist Investing Deep Dives, a separate paid service.

For less than $25 per month, you can join corporate executives, professional money managers, and students of value investing receiving 10-12 issues per year. In addition, you’ll gain access to the archives, now 33 issues and growing! Other benefits include access to a live Berkshire Hathaway sum-of-the-parts valuation model, private subscriber-only Google Meetups, and subscriber introductions.

What follows are excerpts from the January 2024 issue of Watchlist Investing Deep Dives service. Subscribe to read the full issue.

Introduction

Mainfreight came on my radar thanks to Jessie Rancourt, a friend and fellow value investor, who mentioned it during a subscriber meetup a few months ago.

Mainfreight is in the supply chain logistics industry, an extremely broad category covering a huge segment of the world economy and harboring (pun intended) many niches and specialties. I decided a look at the company would fit in well with my coverage of Old Dominion Freight Line (ODFL | Disclosure: None) in the U.S. less-than-truckload space and Triumph Financial (TFIN | Disclosure: Long) in the banking-cum-truckload finance space.

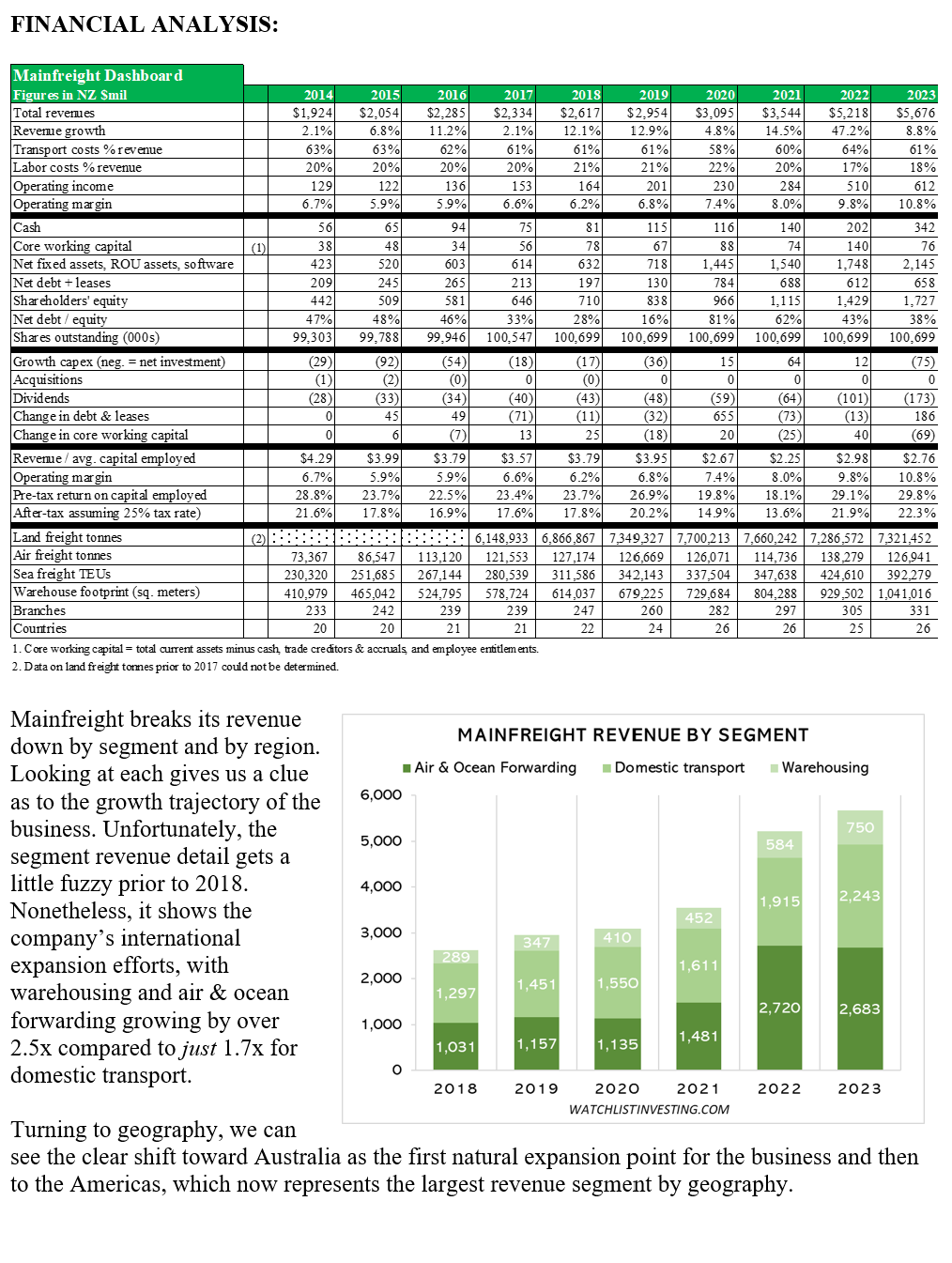

Mainfreight is based in New Zealand with offices around the world and provides shipping services to companies primarily in customer verticals such as food, beverage, DIY, pharmaceuticals, perishables, and retail. Its three segments give a good idea of how it makes money: transport (via road and rail, sometimes with its own fleet), air & ocean (contracting with other service providers), and warehousing (though its own or contracted space).

The company is run by its founder and appears to have maintained a decentralized, entrepreneurial culture. I like what I see in the numbers, in management, and the fact that it is an interesting combination of network benefits and semi-capital intensity. There’s also ample room for reinvestment and a long runway ahead. It is a worthy addition to the Watchlist.

INDUSTRY OVERVIEW:

The worldwide market for shipping / logistics services is huge at about $10.7 trillion or 10% of world GDP in 2023. Third-party logistics services, like those provided by Mainfreight, account for $1.3 trillion worldwide, still a huge number. Safe to say that the market is highly competitive and not subject to control by just a handful of competitors, though there are some very large players. Demand for services depends on world GDP and cross-border trading volume. E-commerce is a driving factor in the industry.

One measure of worldwide pricing of logistics services is the Baltic Dry Index. The spike in mid-2021 is evident no matter what index you use. Pandemic-induced demand caused havoc on the global supply chain and resulted in delays and prices going through the roof.

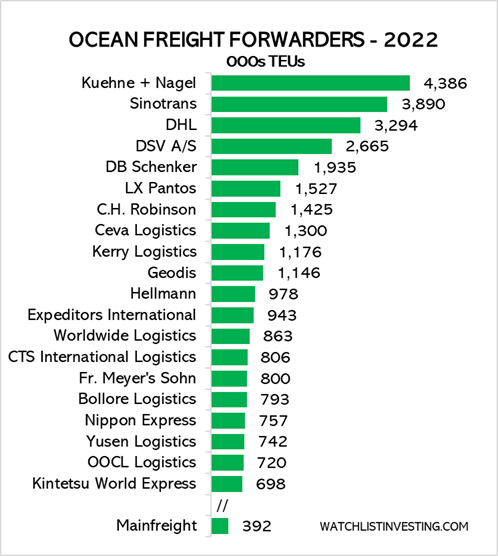

Ocean Freight: Measured in TEUs (twenty-foot equivalent units), ocean freight forwarding volume worldwide was around 67 million units. Note that the global volume for total TEUs through all ports was 851 million units in 2021. Globally, the capacity of container ships has increased from 11 million dwt (deadweight tons) in 1980 to 26 million dwt in 1990; 64 million dwt in 2000; 169 million dwt in 2010; 275 million dwt in 2020, and 293 million dwt in 2023.

In 2023, Mainfreight moved 0.43 million TEUs over ocean (ranking 29th) while Kuehne + Nagel, the largest, moved 4.39 million. C.H. Robinson, by contrast, ranked 7th with 1.43 million TEUs.

Air Freight: The global air freight market was forecast to be about 57.7 million metric tons in 2023. In dollar terms it is valued at approximately $142 billion.[1] Kuehne + Nagel again ranks first in air freight while Mainfreight comes in at 28th.

Land Freight: Global land freight statistics are hard to come by and not as relevant as regional or local statistics. In 2022, Mainfreight moved 7.3 million tons of freight over land.

Warehouse Space: Mainfreight had just over 1 million square meters of warehouse space at the end of 2022. This compares to K + N having 10.3 million square meters. Here K + N ranks 15th while Mainfreight doesn’t even make the list. The industry leader for dry storage warehouses is DHL with 150 million square feet across 520 warehouses. Second is Ryder Supply Chain Solutions with 95 million square feet and over 300 warehouses.

…

…

::: END TEASER:::

I go on to talk about valuation, risks, and present the summary financials from 2014 to 2023 along with other ratios and metrics.

Stay rational! —Adam

Want more in-depth and focused analysis on good businesses? Check out some sample issues of Watchlist Investing Deep Dives, a separate paid service.

For less than $25 per month, you can join corporate executives, professional money managers, and students of value investing receiving 10-12 issues per year. In addition, you’ll gain access to the archives, now 33 issues and growing! Other benefits include access to a live Berkshire Hathaway sum-of-the-parts valuation model, private subscriber-only Google Meetups, and subscriber introductions.