53: Storm Clouds On The Horizon; Analyzing The S&P 500.

Yesterday's good results bode ill for future returns

You’re reading the weekly free version of Watchlist Investing. If you’re not already subscribed, click here to join 1,100 others.

Want more in-depth and focused analysis on good businesses? Check out some sample issues of Watchlist Investing Deep Dives.

For less than $17/month, you can join corporate executives, professional money managers, and students of value investing receiving 10-12 issues per year. In addition, you’ll gain access to the growing archives.

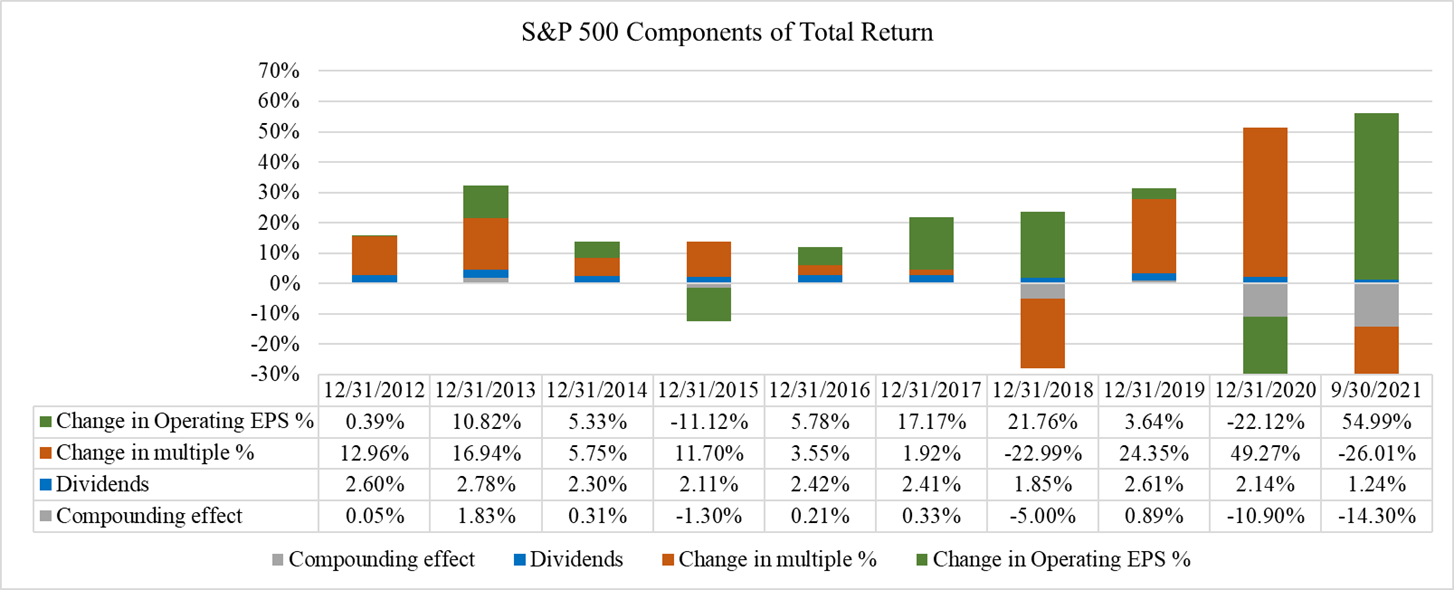

A closer look at the S&P 500

The Standard and Poor’s website provides some interesting raw data on the index, open for anyone to see. These include operating earnings, net earnings, dividends, buybacks, and data on book value, among many other data points. A closer look is very illuminating.

A few observations with updated data through September 30, 2021 (the latest available):

The price/earnings ratio continues a multi-year climb. Excluding the pandemic year of 2020, at 22.7x trailing twelve-month earnings, it is the highest ratio in the periods under analysis. Record-low interest rates rationalize a high P/E ratio. But that party may be about to end if it isn’t already in the beginning stages of doing so.

The balance sheet of the S&P 500 as a whole continues to deteriorate. Debt-to-equity and debt-to-total capitalization are both up compared to 2019 and the highest under this analysis.

The last negative total return for the S&P 500 was in 2018 when it declined a modest 4.38%. One has to look back to 2008 to find the last double-digit decline, which was 37%. It’s not unreasonable to assume that a whole generation of investors don’t know what a real sustained bear market looks like (and probably haven’t taken the time to study history). Trendy investment “strategies” such as “swing trading” or “momentum investing” are just euphemisms for speculation in a market that’s largely been very forgiving compared to its history.

Some thoughts on what this all means for future returns:

If inflation and/or a return to normal interest rates persist, equity returns may well be negative over the next ten years as multiples revert. This may happen in spite of underlying earnings growth.

It seems highly improbable that total returns in the future match or even come close to the S&P 500 total return of 28.7% in 2021. That would require a large upswing in earnings and/or a valuation change. For the index to return even 10% from its point in September 2021, earnings would have to come in at $209 with the same 22.7x multiple of earnings. Conversely, the price/earnings multiple would have to increase to 25x. Or some combination of the two. I’m not saying it can’t happen (anything can happen in markets over the short run) only that it’s unlikely. We’re in an area of the curve that’s asymptotic (approaching zero)—it’s inherently unstable.

Compounding the valuation risk above is balance sheet risk. The companies in the index are collectively more highly leveraged than seven or eight years ago.

In short, the trends in the index over the past half-decade or so are unsustainable. Trees cannot grow to the sky. Given today’s low interest rate environment and valuations at present levels, annual returns over the coming decade are highly unlikely to reach double digits, in my opinion.

Note: The S&P 500 total return for calendar year 2021 was 28.7%.

If you enjoyed this post I’d appreciate you taking a moment to help me spread the word by sharing it. Thank you!

Stay rational! —Adam

P.S. Cover Photo by Tasos Mansour on Unsplash