65: Examining Berkshire's 2003 Acquisition of McLane from Walmart; Do Margins Matter?

Excerpt from BRK book and Warren Buffett video

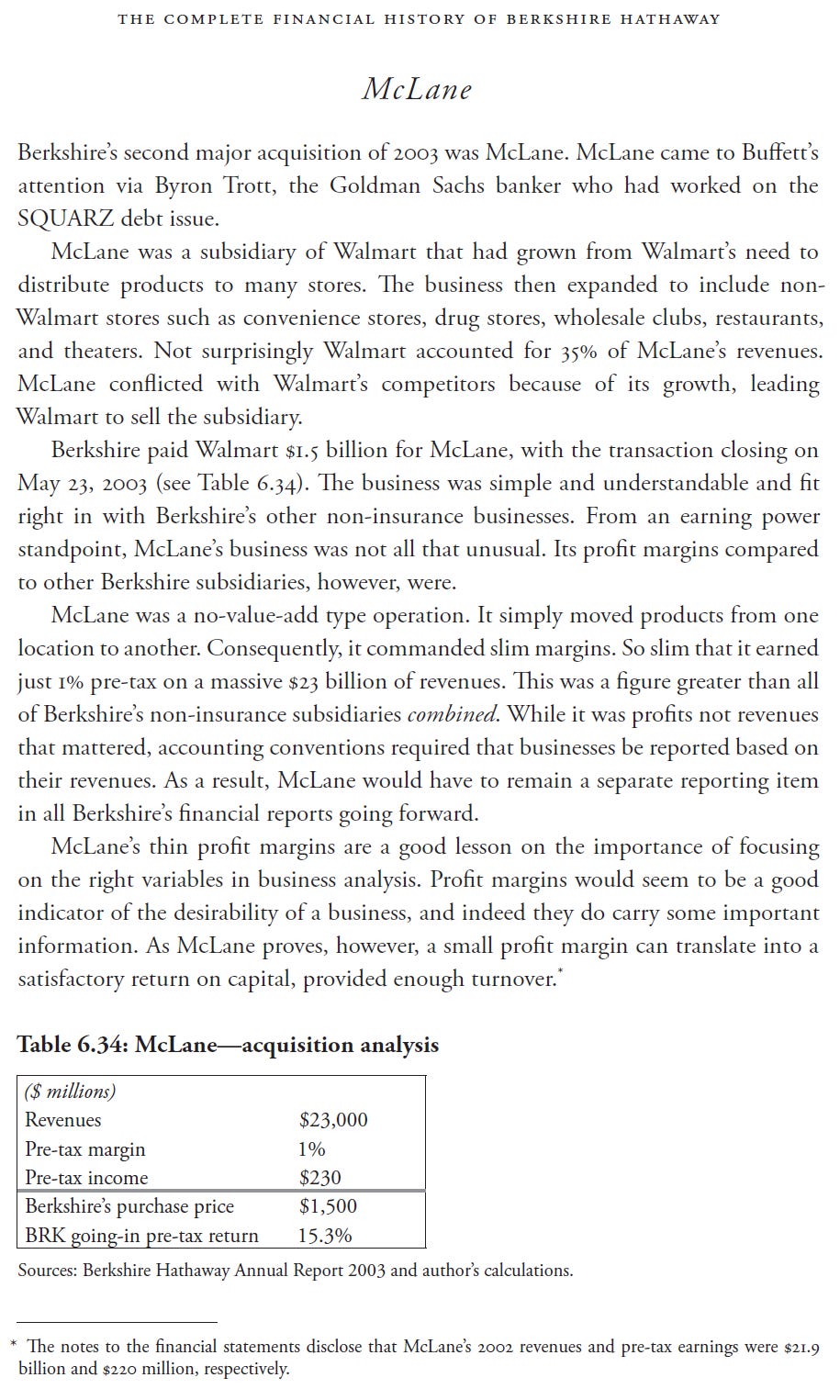

McLane

McLane is a distributor who sits between powerful suppliers and customers. As a consequence, it commands very low margins, as low as 1% pre-tax at the time of Berkshire’s purchase in 2003. BRK bought the company from Walmart for $1.5 billion.

How can a 1% margin be representative of a good business? In a word, turnover. At the time of purchase, McLane had annual revenues of $23 billion. A 1% margin on that level of sales translated into $230 million of pretax earnings, and a return of 15.3% pre-tax on Berkshire's purchase price. McLane's margins have declined even further over the years due to competition.

Coincidentally, in 2021, McLane earned $230 million on revenues of almost $50 billion, a margin of 0.47%. It's still a fairly good business, and Berkshire has received lots of earnings over the years. It's just not as good as when BRK first purchased it.

Here’s more on McLane from my book: