Gencor Industries (#6)

Hidden Value or Value Trap?

Note: The following was first published in the May 2021 paid issue of Watchlist Investing. Nothing herein should be considered investment advice or an offer to buy/sell securities.

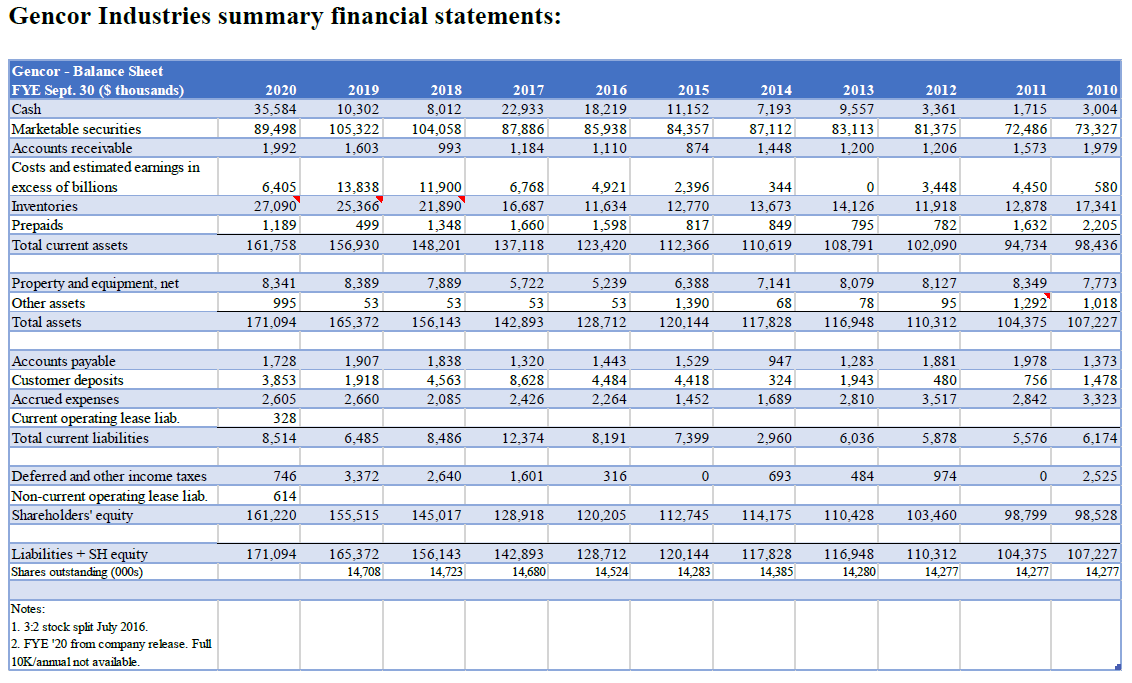

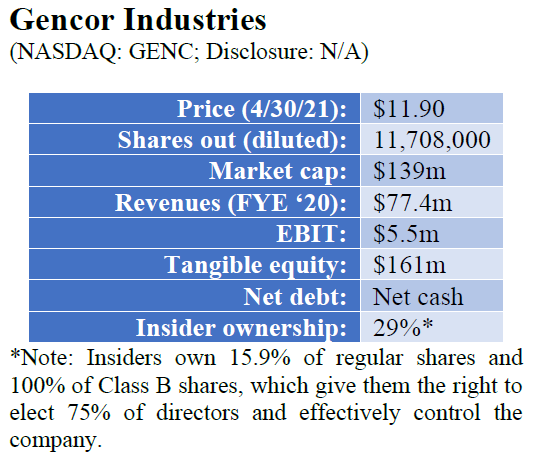

GENC has $125m (78% of its equity and 90% of its market cap) in cash/marketables.

Gencor operates in the heavy machinery business. It manufactures asphalt plants and related equipment for road construction. Not surprisingly, the industry is characterized by cyclicality as highway funding bills are passed or defeated and as projects wax/wane. While cyclical, the business/industry does benefit from the fact that asphalt isn’t going away anytime soon.

I came across GENC while sorting the list of Russell 3000 companies for nonbank companies that might get excluded from the index upon rebalancing. That sort found 15 companies in four sectors that appeared to be good prospects for future study. One of those was GENC. I was attracted to the small market cap, high insider ownership, and huge net cash position.

Upon further digging my excitement waned as I realized the company had the potential to be a value trap. High insider ownership is a good thing, but not if it comes at the cost of drifting into sub-par capital allocation. GENC has $125m (78% of its equity and 90% of its market cap) in cash/marketables. While part of that is a good thing considering GENC operates in a cyclical industry, the amount appears excessive.

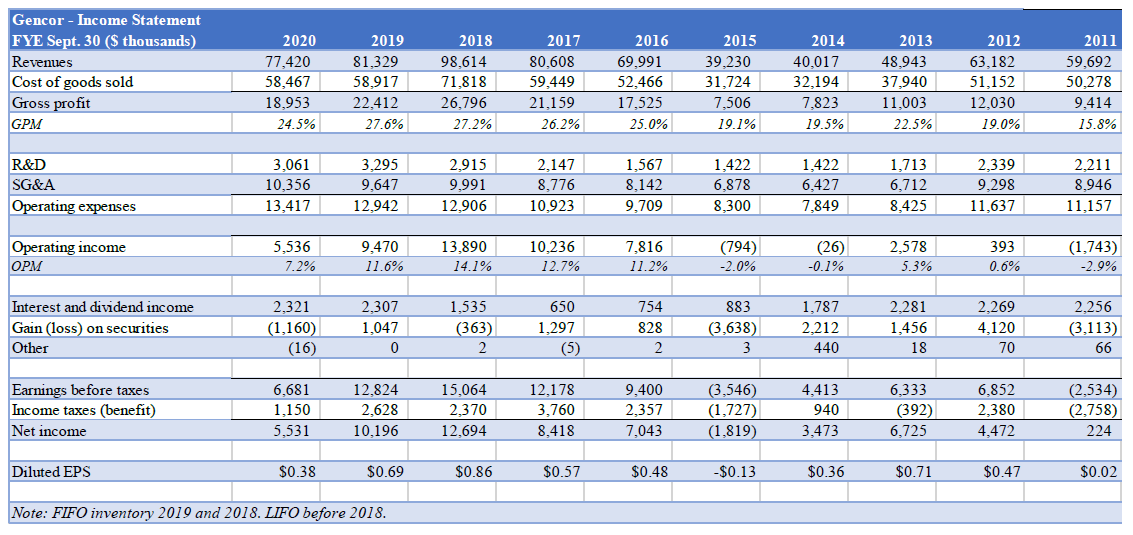

GENC doesn’t pay a dividend and hasn’t been a repurchaser of its own shares. That seems to be a mistake. Shares traded between 67% and 100% of book value between 2011 and 2015. Management could have (should have) repurchased undervalued shares while still maintaining liquidity to ride out cyclicality and provide dry powder for acquisitions.

In October 2020 GENC purchased a paving equipment business from Volvo for $14.4m. Very little is known about the business other than it was apparently purchased at book value (inventories of $11m + fixed assets of $3.4m).

GENC is run by the Elliott family. Chairman, E.J. Elliott is 91, and his sons Marc and John hold the president and CEO titles, respectively. Through my research I found out CFO, Eric Mellen, is E.J.’s son-in-law, although I couldn’t independently verify that.

In my research, I came across this in-depth article written by a forensic accountant which chronicles various attempts by outsiders to gain seats on the board and extract value from the business. It also points toward some misdeeds by company management and insiders beginning about 25 years ago. While it appears the misdeeds are largely behind the company, the fact that this past does exist might be a reason for pause.

Something might happen to create a catalyst event. The passing of the 91-year-old current chairman could be such an event, but that isn’t imminent or certain, especially given the Class-B control shares. Perhaps the next generation of Elliotts can be persuaded to buy back shares if/when they trade below book value. Or they might desire more cash for themselves and pay a dividend (or they could start paying themselves rich salaries, which is always a risk).

To sum up, GENC appears to be a decent cyclical business controlled by insiders who have resisted outside attempts to change its ways. GENC is one of those companies to maintain on the Suspect List to keep an eye on but is a pass right now given too many unknowns and possible issues.