25: Old Dominion Freight Line (ODFL)

ODFL is a wonderful, easy-to-understand business with competitive advantages

Watchlist Investing was never intended to be a source of always-timely or immediately actionable investment ideas. Rather, my goal has been to follow Charlie Munger’s advice1 in building a list of great companies to follow, secure in the knowledge that opportunities to jump in at attractive prices will materialize in the future.

This concentrates my research on finding and understanding good businesses regardless of their current valuation. Each month the list of case studies grows larger and subscribers to the full paid version have access to this growing valuable resource.

Subscribers can earn back the nominal cost of subscribing in just one issue. How? It takes 40+ hours of reading, researching, thinking, and writing to produce one W.I.N. newsletter. You can digest it all in less than an hour saving huge amounts of time.

Join the growing list of value investors, C-Suite execs, managers, and students by subscribing. I think it’s worth full price but as an enticement to you, my Substack readers, I’ll give you 10% off your first year. Use the code “Substack” at checkout.

Old Dominion (ODFL; Disclosure: None) is a great business I’ve simply overlooked—and underappreciated. Having missed the boat…er, truck…for too long I thought I’d do a deeper study of the company.

What I found was a wonderful, relatively simple business operating in a tough industry. ODFL has gotten ahead by figuring out how to move freight from Point A to Point B (and beyond) in an efficient manner.

The family-controlled business built its capabilities intentionally, rationally, and methodically over several decades. The capital-intensive nature of the business might not seem as exciting or profitable as other segments of the freight industry, but it serves as a formidable protective barrier to entry.

ODFL is a company worth understanding and deserves a spot on the Watchlist.

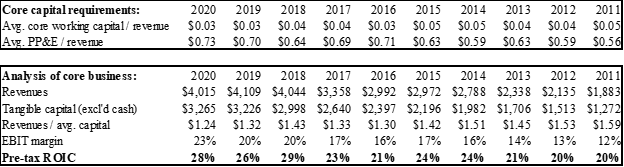

Pretty much all the “action” is concentrated in fixed assets. Companies in the industry require little to no working capital. At first glance, it might look like the growing capital intensity (as seen in average PPE/revenue and revenues/avg capital) is a bad thing. But ODFL has invested in technology and systems which have allowed it to operate more efficiently and generate higher margins and by extension higher returns on capital…

Strong returns on capital have allowed ODFL to maintain a pristine balance sheet all the while investing in its business and returning capital to shareholders.

Even with its complexities, LTL (less-than-truckload) is just like full truckload in that it’s all about getting a shipment from Point A to Point B. Both try to move a lot of volume efficiently and accurately. The way each company designs and operates its system determines how profitable it is. Here are the three key metrics I believe drive the business (no pun intended).

Key metric #1: How much total unit volume was moved through the system?

A certain level of volume is necessary for a carrier to have national scale and the ability to benefit from economies of scale or network effects. Volume is measured in tons and in shipments.

Key metric #2: How much tangible capital is required to move that volume?

Key capital requirements are tractors and trailers, and service centers which allow for sorting/routing of shipments. The industry has minimal working capital requirements. A key decision within a system is how much trucking volume to outsource. This has the advantage of lowering capital requirements but at the expense of control and lower margins.

Key metric #3: What is the operating ratio / EBIT margin?

The industry measures efficiency with the operating ratio, which is simply operating expenses divided by revenues. So lower equals better. EBIT margin is what’s leftover and could be a more intuitive way to think about it. There’s a lot packed in this ratio, which includes the carrier’s ability to price its service and its decision on how much volume to move internally.

I chose not to include service center metrics. How many service centers and how they’re used are a key design of an LTL system, but they largely factor into the key metrics above. I hesitated to put the claims ratio in as a fourth key metric, because it’s important but in the end factors into pricing/margins. ODFL has a ridiculously low 0.10% claims ratio compared to a “good” industry target of 0.50%.

We can see the three key metrics at work in the strategies of ODFL and three other near-pureplay LTL carriers, Saia, Inc. (Ticker: SAIA; Disclosure: None), Yellow Corp (Ticker: YELL; Disclosure: None), and ArcBest (Ticker: ARCB; Disclosure: None). See chart below. The strongest correlation is seen between the level of capital intensity and margins.

As more volume is brought in-house by investing in an owned fleet, purchased transportation goes down, and EBIT margins go up. The effect of reducing outsourcing is more than linear because of the advantages gained in efficiencies and accuracy of shipments. This also manifests itself in a degree of pricing power because on-time deliveries free of damage are extremely important to shippers, and the cost of freight is generally a fraction of an item’s overall value.

Subscribers to the paid W.I.N. have access to the full in-depth report, which includes my thoughts on valuation and more.

Stay rational! -Adam

“One person said to me, 'I have a list of 300 potentially attractive stocks, and I constantly watch them, waiting for just one of them to become cheap enough to buy.' Well, that's a reasonable thing to do. But how many people have that kind of discipline? Not one in 100.”

– Charlie Munger

Quality high-level industry research